Table of Contents

Why Most Budgets Fail and How to Pick One That Sticks

Sixty percent of Americans do not follow a written budget, according to a 2023 Debt.com survey. Of those who do, roughly one in three abandon their method within the first six months. The problem is rarely the budget itself. It is a mismatch between the method and the person. A freelancer with irregular income will struggle with the same system that works beautifully for a salaried government employee. Recognizing this is the first step toward building a budget you can actually keep.

Three methods dominate the personal finance conversation for good reason. The 50/30/20 rule is simple enough to remember in your head. Zero-based budgeting gives you total control over every dollar. Envelope budgeting, especially in its cash-based form, delivers a psychological brake on overspending that digital tools cannot replicate. Each one works, but each serves a different type of spender and income pattern.

The practical rule: pick the method that matches your income stability and your relationship with spending. If you change methods and still fail after three months, the issue is likely discipline, not the framework. But if you pick the wrong framework from the start, even high discipline will crumble.

The 50/30/20 Budget: Simple, Flexible, and Hard to Mess Up

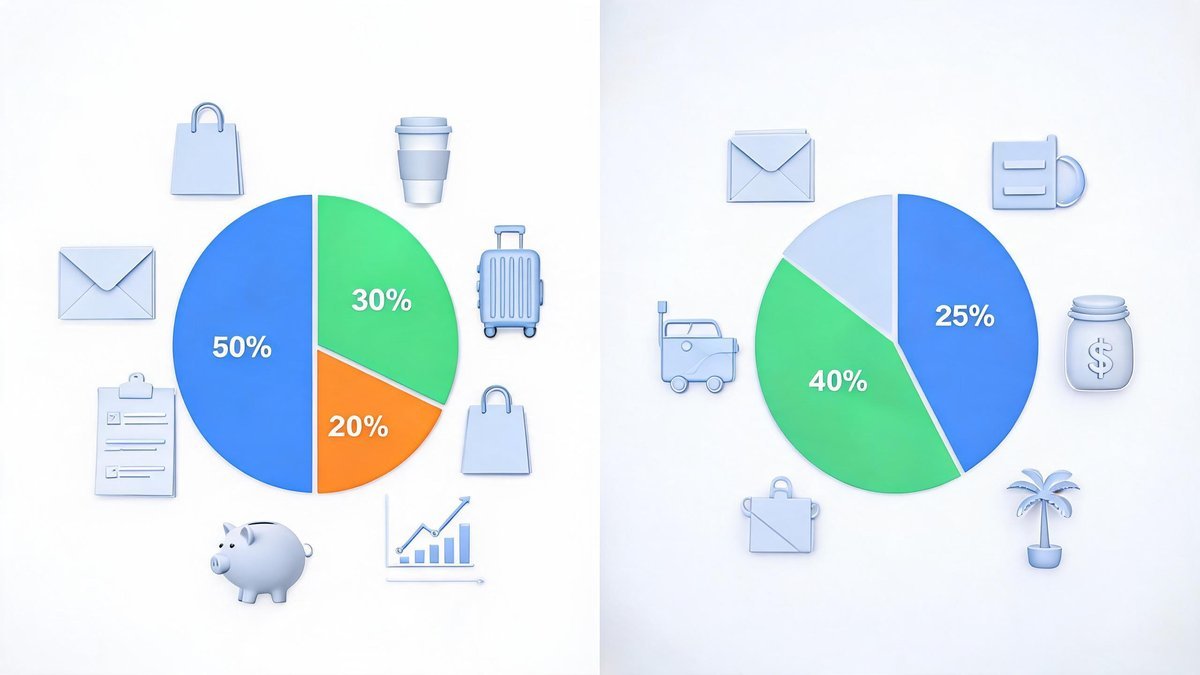

Popularized by Senator Elizabeth Warren in her book "All Your Worth," the 50/30/20 budget splits your after-tax income into three buckets. Fifty percent goes to needs: housing, utilities, groceries, minimum debt payments, and essential transportation. Thirty percent goes to wants: dining out, streaming subscriptions, hobbies, and travel. The remaining twenty percent goes to savings and extra debt payments. The simplicity is the selling point. You do not need a spreadsheet. You do not need to track 30 spending categories.

Financial Fact: The 50/30/20 budget — 50% needs, 30% wants, 20% savings — was popularized by Senator Elizabeth Warren and remains the most recommended budgeting framework for beginners.

This method works best for people with stable, predictable incomes who are not drowning in high-interest debt. If housing alone eats up 45% of your take-home pay, as it does for 22% of renters nationwide according to Harvard's Joint Center for Housing Studies, then 50/30/20 becomes 65/15/20, and you will feel pinched every month. The method also becomes less useful when you want to save aggressively. Saving 20% is solid, but early FIRE seekers aiming for 50% savings rates need a tighter system.

The strengths are real: zero learning curve, sustainable over decades, and built-in permission to spend on wants without guilt. If you have avoided budgeting because it feels restrictive, start here. Use a free app or a simple bank account split to separate the three buckets and check in monthly.

Zero-Based Budgeting: Every Dollar Gets a Job

Zero-based budgeting requires you to assign a purpose to every dollar of your income until your income minus your expenses equals zero. That does not mean you spend everything. It means your savings, investments, and debt payments are also assigned dollars. Dave Ramsey's EveryDollar app and YNAB (You Need a Budget) both use zero-based logic, and YNAB alone claims over 750,000 active users who report an average of $600 in monthly savings improvement after starting.

This method shines for people with variable expenses or financial goals that require surgical precision. If you are paying off $40,000 in student loans while trying to build an emergency fund, zero-based budgeting tells you exactly how much goes to each priority. It also forces you to confront wasteful spending. When you have to manually assign $12 to a forgotten subscription, you either keep it consciously or cancel it. Most people cancel.

The downside is the time investment. You need to update the budget at least weekly, and ideally you check it before every discretionary purchase. This friction causes about 40% of new zero-based budgeters to quit within three months, according to user retention data shared by budgeting app developers. The fix: carve out 15 minutes every Sunday evening for a budget check-in. Treat it like a standing meeting with yourself. After two months, the habit solidifies and the time cost drops.

For couples, zero-based budgeting works especially well because it forces explicit conversation about priorities. Instead of arguing about a random Amazon purchase, you both agree on the spending plan at the start of the month and execute it together. According to a Ramsey Solutions study, couples who budget together report 38% fewer money arguments.

Envelope Budgeting: The Cash-Based Method That Actually Curbs Spending

Envelope budgeting is the oldest method and arguably the most behaviorally effective. You withdraw cash for each spending category at the start of the month, place it in labeled envelopes, and when an envelope is empty, you stop spending in that category. Research from the Journal of Consumer Research confirms that people spend 12% to 18% less when using physical cash versus credit cards. The pain of handing over bills triggers a psychological response that swiping plastic does not.

You do not have to use physical cash anymore. Apps like Goodbudget and Qube Money digitize the envelope system, creating virtual envelopes that track spending in real time. Goodbudget's free tier gives you 20 envelopes, and their paid plan at $8 per month adds unlimited envelopes and account syncing. These digital versions preserve the core concept while accommodating online shopping and recurring bills.

The envelope method excels for people who overspend in specific categories. If you routinely blow $400 on dining out when your target is $200, a dedicated restaurant envelope with a hard limit forces a decision every time you reach for that envelope. It also builds what behavioral economists call "mental accounting," where money feels different depending on its labeled purpose. This is technically irrational, because dollars are fungible, but it works. Studies by behavioral finance researchers show that mental accounting increases savings rates by 8% to 15% compared to treating all money as one pool.

The limitation: envelope budgeting is awkward for irregular expenses like car repairs or annual insurance premiums. You need sinking funds, separate envelopes where you accumulate money each month for predictable-but-irregular costs. This adds administrative overhead that the 50/30/20 method avoids entirely.

How to Combine Methods for Maximum Results

You are not limited to one system. Many successful budgeters use a hybrid. One effective combination pairs zero-based logic for fixed expenses and savings with envelope-style limits for discretionary categories like dining, entertainment, and clothing. The fixed side runs with surgical precision. The discretionary side gives you flexibility within hard caps. A 2023 survey by the budgeting app Monarch Money found that 44% of its users combined at least two methods, and those users reported 22% higher savings rates than single-method users.

Another hybrid starts with 50/30/20 as the top-level framework, then applies zero-based detail only to the "wants" bucket. This keeps the big picture simple while addressing the categories where most people leak money. You can also reverse-engineer your ideal method: identify the one spending category that causes the most trouble each month, apply the strictest method to it alone, and stay loose with everything else. Success in one category often builds the confidence to expand the system.

The practical rule: pick one method, run it for 90 days without modification, then adjust. The worst budgeting method is the one you stop using. The second-worst is the one you keep switching every month. Commit, execute, review, then tweak.

Building a robust savings habit is the foundation of financial independence, yet most people never develop a systematic approach to saving. The most effective strategy is to automate your savings so the money moves out of your checking account before you have a chance to spend it. Setting up an automatic transfer on payday to a dedicated savings account removes the willpower element entirely. Financial advisors typically recommend saving at least 15 to 20 percent of your gross income for long-term goals. If that seems impossibly high, start with 5 percent and increase it by one percentage point every three months. The gradual ramp-up is barely noticeable in your daily spending but produces dramatic results over a working career due to the power of compound growth.

Investing does not require a finance degree or hours of daily research. A straightforward approach using low-cost index funds or ETFs that track broad market indices has historically outperformed the majority of actively managed funds over any ten-year period. The key principles are simple: diversify across asset classes, keep costs low, reinvest dividends automatically, and stay invested through market ups and downs. Attempting to time the market -- selling before downturns and buying before rallies -- is a losing strategy even for professional investors. The single most important factor determining your investment success is not which stocks you pick but how long you stay invested. Time in the market beats timing the market nearly every time over meaningful investment horizons.

Your credit score affects far more than your ability to get a loan. Landlords check credit before approving rental applications, insurance companies use credit-based scores to set premiums, and some employers review credit reports during the hiring process for certain positions. Maintaining a strong credit profile requires consistent habits: paying all bills on time every month, keeping credit card utilization below 30 percent of your available limit, maintaining a mix of credit types, and avoiding unnecessary credit inquiries by only applying for new accounts when genuinely needed. Reviewing your credit reports annually from all three major bureaus through AnnualCreditReport.com helps you spot errors or fraudulent activity before they cause significant damage to your score.