Table of Contents

- 1. Understanding the Core Tax Difference

- 2. When Your Current Tax Bracket Points the Way

- 3. The Power of Tax-Free Growth Over Decades

- 4. Income Limits and the Backdoor You Should Know About

- 5. Required Minimum Distributions: The Rule That Ages Differently

- 6. The Hybrid Approach: Why You Don't Have to Pick Just One

You're staring at two retirement account options, and they sound almost identical until you dig in. Roth IRA. Traditional IRA. Both let your money grow without a yearly tax drag. Both come with the same contribution ceiling. But the way they treat your tax bill—that's where the real story unfolds. Pick wisely, and you'll keep tens of thousands more in your pocket over a 30-year retirement. Pick without thinking, and you might owe the IRS far more than necessary.

This isn't about which account is "better" in some abstract sense. It's about which account fits your income trajectory, your tax situation today, and the lifestyle you want three decades from now. Let's walk through the decision step by step, with real numbers you can apply before you make your next contribution.

1. Understanding the Core Tax Difference

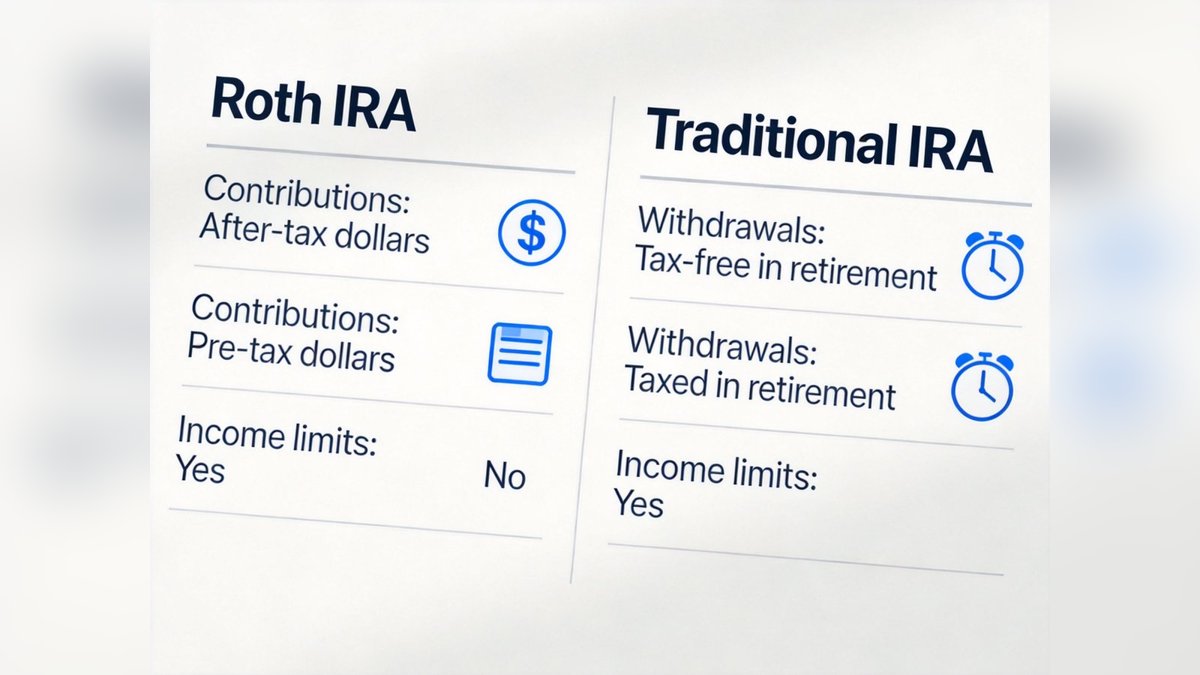

The fundamental split between these two accounts comes down to one question: do you want your tax break now, or do you want it when you retire? With a Traditional IRA, you contribute pre-tax dollars. The money goes in, you deduct it from your taxable income this year, and your tax bill shrinks immediately. A single filer in the 22% bracket who contributes the full $7,000 saves $1,540 on their taxes that same spring. Then the account grows. Then you retire. Then every withdrawal gets taxed as ordinary income. The IRS gets its cut eventually—it just waits.

A Roth IRA flips that sequence completely. You contribute money you've already paid taxes on. No deduction shows up on this year's return. But when you're 65 and pulling money out, every dollar—contributions, earnings, dividends, all of it—comes to you tax-free. For 2025, the contribution limit for both accounts sits at $7,000, with a $1,000 catch-up allowance if you're 50 or older. That's $8,000 total you can shelter each year. The question isn't whether to save. It's which tax timeline serves you better. If you expect your tax rate to climb over your career, paying taxes now at a lower rate and withdrawing tax-free later tilts the math toward Roth. If you're in your peak earning years and your tax rate feels punishing, the immediate deduction from a Traditional IRA might give you more breathing room today.

2. When Your Current Tax Bracket Points the Way

Your marginal tax rate right now is the single most useful number in this decision. If you're early in your career and solidly in the 12% federal bracket—which in 2025 covers single filers with taxable income up to roughly $48,475—a Roth IRA becomes very hard to argue against. You pay 12% now, and decades of compounded growth emerge completely untaxed. That's a bargain that's tough to beat. The math shifts significantly once you cross into the 22% bracket, which for 2025 stretches from about $48,476 to $103,350 for single filers. At that level, a $7,000 Traditional IRA contribution knocks $1,540 off your federal tax bill. That's real money you can reinvest, use to pay down debt, or funnel into a taxable brokerage account.

Financial Fact: Term life insurance for a healthy 30-year-old costs roughly $20-$30/month for $500K coverage. Whole life policies cost 10-15x more and mix insurance with underperforming investment products.

Here's the practical takeaway most people miss: don't just look at your salary. Look at your taxable income after deductions. A married couple earning $130,000 who max out two 401(k) plans and claim the standard deduction might drop their taxable income well into the 12% bracket. At that point, Roth contributions suddenly make a lot more sense than they did at first glance. Run your numbers through a tax estimator before you commit. And if you're self-employed with a variable income, consider making your IRA contribution decision later in the year when you have a clearer picture of which bracket you'll actually land in.

3. The Power of Tax-Free Growth Over Decades

Time is the Roth IRA's best friend, and the longer you give it, the more dramatic the advantage becomes. Say you're 30 years old and you put $500 a month into a Roth IRA. At a 7% average annual return—roughly in line with the S&P 500's inflation-adjusted historical performance—you'd have about $567,000 by age 65. In a Roth, every penny of that belongs to you. In a Traditional IRA, you'd owe income tax on every withdrawal, which at a 22% effective rate would cost you nearly $125,000 over the course of retirement. That's the cost of deferring taxes rather than paying them upfront.

Even a shorter timeline benefits from tax-free compounding. Someone who starts at 45 and contributes $7,000 annually until 65, earning the same 7%, would accumulate roughly $287,000. In a Roth, that's $287,000 net. In a Traditional account, the after-tax value drops to around $224,000 at a 22% rate. The gap narrows with fewer years, but it never disappears. The actionable piece here: if retirement is more than 15 years away, give serious weight to the Roth. The tax-free growth engine simply has more runway to do its work. And remember—nobody knows what tax rates will look like in 2045. A Roth locks in today's rates. A Traditional IRA leaves you exposed to whatever Congress decides later.

4. Income Limits and the Backdoor You Should Know About

Not everyone can waltz into a Roth IRA. The IRS draws a line based on your modified adjusted gross income, and if you're above it, direct contributions get reduced or eliminated entirely. For 2025, the phase-out range for single filers starts at $150,000 and ends at $165,000. For married couples filing jointly, it stretches from $236,000 to $246,000. Earn a dollar above the top of that range, and your Roth contribution limit drops to zero. Traditional IRAs, by contrast, have no income limits on contributions. Anyone with earned income can contribute to a Traditional IRA, even if the deduction itself might be limited if you or your spouse has a workplace retirement plan.

But the backdoor Roth IRA strategy exists for a reason, and it's perfectly legal. You contribute to a Traditional IRA (non-deductible, since your income is too high), then convert that balance to a Roth IRA shortly afterward. You'll owe taxes on any pre-conversion earnings, but if you convert quickly, those are minimal. Roughly 6% of IRA-owning households use the backdoor Roth strategy, according to industry data. The catch: if you have existing pre-tax IRA balances, the pro-rata rule complicates the math. Consult a tax professional before attempting it. For most high earners, though, the backdoor Roth keeps the tax-free growth option on the table even when the front door is locked.

5. Required Minimum Distributions: The Rule That Ages Differently

Here's a difference that doesn't matter at 35 but matters enormously at 75. Traditional IRAs come with required minimum distributions—the IRS forces you to start withdrawing money whether you need it or not. Under the SECURE Act 2.0, RMDs now begin at age 73 for those born between 1951 and 1959, and at age 75 for those born in 1960 or later. The government wants its tax revenue, and it won't wait forever. If your Traditional IRA balance hits $800,000 at age 75, your first RMD would be roughly $32,000, all taxable. That forced withdrawal can push you into a higher bracket, increase your Medicare premiums through IRMAA surcharges, and make more of your Social Security benefits taxable.

Roth IRAs, by contrast, have no RMDs during the original owner's lifetime. None. You let the money sit and compound as long as you want. This makes Roth accounts powerful estate-planning tools—your heirs will have to take distributions, but those withdrawals come out tax-free. If you don't anticipate needing your full IRA balance to live on, the Roth's flexibility becomes a genuine strategic advantage. The practical move: if you're already on track with your retirement savings and expect to have surplus, favor the Roth. The absence of forced withdrawals preserves your ability to control your taxable income in retirement, which keeps you in lower brackets and avoids surprise tax bills.

6. The Hybrid Approach: Why You Don't Have to Pick Just One

Too many articles frame this as an either-or decision, and that's a mistake. You can split your $7,000 contribution between both account types in whatever proportion makes sense for your situation. Maybe you put $4,000 in a Traditional IRA to capture some immediate tax savings and drop your adjusted gross income below a key threshold, then put the remaining $3,000 in a Roth to build your tax-free bucket. About 35% of IRA-owning households hold both types, and for good reason—tax diversification is just as valuable as asset diversification.

Consider a 40-year-old in the 22% bracket who isn't certain whether their retirement tax rate will be higher or lower. By splitting contributions, they hedge the bet. If taxes rise, the Roth portion shields them. If taxes fall, the Traditional contributions were the smart play. They also gain flexibility: in retirement, you pull from the Traditional IRA to fill the lower tax brackets, then tap the Roth for larger expenses without bumping into a higher marginal rate. This tax-bracket management strategy can extend the life of your portfolio by several years. As of 2025, roughly 43 million U.S. households own IRAs, and those who diversify across account types report greater confidence in their retirement readiness. The split doesn't have to be 50/50. Tilt it based on your bracket today, your expectations for the future, and how much control you want over your taxable income in your 70s and 80s.

The Roth versus Traditional decision rewards people who take an honest look at their current tax situation and make a clear-eyed forecast about the future. You don't need a crystal ball. You need your most recent tax return, a rough idea of your career earnings trajectory, and a willingness to revisit the choice each year as circumstances shift. Start there, and you'll land on the right mix.